Asset allocation is one of the most important elements of an investment strategy. It refers to how investments are divided among different asset classes, such as stocks, bonds, and cash. The goal of asset allocation is to balance potential growth with risk management in a way that supports long-term financial goals.

As individuals move through different stages of life, their investment priorities, time horizons, and risk tolerance may evolve. Because of this, asset allocation often changes gradually over time.

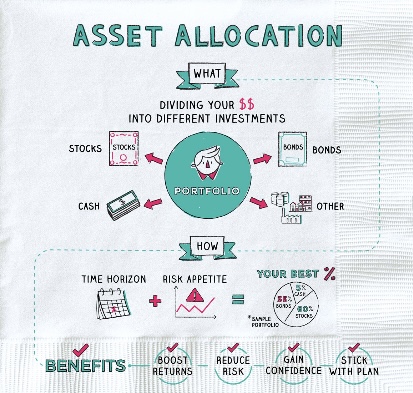

What Is Asset Allocation?

Asset allocation describes the mix of investments within a portfolio. Common asset classes include:

- Stocks – often associated with long-term growth potential

- Bonds – typically used to provide income and stability

- Cash or cash equivalents – used for liquidity and short-term needs

Each asset class behaves differently during changing market conditions. By diversifying investments across these categories, investors may reduce the impact of volatility on their overall portfolio.

Asset allocation is generally considered one of the most important drivers of long-term investment outcomes.

Asset Allocation in Your 20s and 30s

During the early stages of a career, many investors have a long time horizon before retirement. This extended time frame often allows for greater exposure to growth-oriented investments.

At this stage, investors may focus on:

- building long-term wealth through consistent investing

- contributing regularly to retirement accounts

- maintaining a diversified portfolio

- taking advantage of time in the market

Because retirement may still be decades away, short-term market fluctuations may have less impact on long-term goals.

Asset Allocation in Your 40s and 50s

As individuals move into mid-career, financial responsibilities often expand. This may include:

- supporting a family

- paying for education expenses

- managing mortgage payments

- increasing retirement savings

During this phase, many investors begin balancing growth opportunities with increasing portfolio stability.

Asset allocation adjustments during this stage may involve gradually increasing diversification and evaluating how investment risk aligns with long-term goals.

Regular portfolio reviews often become more important as retirement approaches.

Asset Allocation in Your 60s and Beyond

As retirement nears or begins, the investment focus often shifts toward income generation and capital preservation.

Many retirees depend on their portfolios to help support spending needs, which may lead to adjustments in asset allocation.

Key considerations during this stage may include:

- managing market volatility

- supporting retirement income needs

- maintaining sufficient liquidity

- coordinating investment strategy with withdrawal planning

Even in retirement, however, many portfolios still maintain some exposure to growth-oriented assets to help support long-term purchasing power.

The Importance of Diversification

Regardless of age, diversification remains an important component of investment strategy.

Diversification involves spreading investments across different asset classes and sectors to reduce the impact of any single investment on the overall portfolio.

While diversification cannot eliminate risk, it may help investors navigate changing market conditions more effectively.

Asset Allocation Is Not One-Size-Fits-All

Although age is often used as a general guideline for asset allocation, individual circumstances can vary significantly.

Factors that may influence asset allocation include:

- retirement timeline

- income stability

- financial goals

- risk tolerance

- other financial resources

Because these factors differ for each household, investment strategies are often tailored to reflect personal financial situations rather than relying solely on age-based rules.

Aligning Investments With Long-Term Goals

Asset allocation should ultimately support broader financial goals rather than simply following a formula.

When investment strategy is aligned with long-term priorities—such as retirement income, financial independence, and lifestyle goals—it becomes easier to maintain discipline during changing market conditions.

A thoughtful financial plan helps ensure that investment decisions support both financial security and the experiences that matter most throughout life.

Final Thoughts

Asset allocation is a key element of long-term investing and often evolves over time as financial goals and circumstances change. By understanding how investment strategy may shift throughout different stages of life, individuals can approach their portfolios with greater clarity and confidence.

A well-structured financial plan can help ensure that asset allocation decisions remain aligned with both short-term needs and long-term objectives.

Considering Financial Planning?

If you’re thinking about retirement, taxes, investments, or other important financial decisions, a conversation may help clarify your next steps.

Continue Reading

Retirement planning involves several variables including taxes, investment strategy, and spending assumptions.

About Weiss Financial Group

Keith Weiss is a financial planner and principal of Weiss Financial Group, serving individuals and families throughout Westchester County, Putnam County, and nearby Connecticut communities.

Leave a comment